Employee Stock Option Plans (“ESOP”) have long been a popular tool for companies to attract, retain, and motivate employees. The idea is simple: give employees a stake in the company’s ownership, and they will work harder and stay longer. On paper, it sounds like a win for everyone.

But in practice, ESOP resolutions at shareholder meetings have become one of the most debated topics in Indian corporate governance. A growing number of institutional investors — mutual funds, pension funds, foreign investors, and insurance companies — are voting against these resolutions, sometimes in very large numbers.

This blog seeks to present both perspectives:

- Why institutional investors believe their concerns remain valid when voting against ESOP resolutions; and

- why companies believe they are acting in full compliance with the law and in the best interests of their employees despite significant opposition.

The objective is to better understand this gap and explore ways to bridge it.

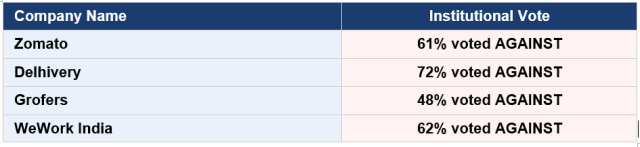

1. The Scale of Institutional Opposition

Before diving into perspectives, consider how institutional investors have voted on ESOP resolutions at some well-known listed companies:

Ironically, most of these resolutions were still approved. Why? Because promoters and retail shareholders had enough votes to pass them even without institutional support.

So, the question is not just about whether the resolution is passed. It is about what these voting patterns tell us about a gap in understanding between investors and companies.

2. The Investor’s Point of View: Why they Vote Against ESOP Resolutions

Institutional investors are not against ESOPs as a concept. In fact, most of them actively support well-designed ESOP schemes. What they object to is how some schemes are structured and explained.

- Shareholders Bear the Cost of Every New Share Issued

When employees exercise their options and receive shares, those shares are usually newly issued by the company. That means the total number of shares in the market goes up and when that happens, every existing shareholder’s stake gets smaller — this is called dilution.

Investors are not against paying employees well but they want to know:

- how much dilution are we accepting?

- For what benefit?

- For which employees?

If a company cannot answer these questions clearly, investors will vote against it.

- Deep Discounts on Exercise Price Feel Like a Direct Transfer of Wealth

The exercise price is the price at which an employee can buy the company’s share in the future.

For example: If the current market price is ₹500 and the exercise price is set at ₹1(i.e. face value), an investor would reasonably ask: why are we transferring ₹499 per share in value to employees?

Institutional investors broadly accept discounts of up to around 20% on Current Market Price of the Shares as on date of grant of ESOPs. Beyond that, they see it as shareholder value being transferred to employees without a clear justification and if that justification is not explained in the notice, they will vote against.

- Problem with Purely Time-Based Vesting

Many ESOP schemes vest options simply based on how long an employee stays with the company. Stay for three years, get your shares. Investors find this difficult to support, because it rewards presence, not performance.

If the company has not grown, if profits have not improved, if targets were missed — why should employees receive shares at a discount? From an investor’s perspective, that is a reward without accountability.

- Concentration of ESOPs among Senior Leadership

Investors are more supportive of ESOP schemes that cover a wide range of employees, not just the top leadership.

When they see that 70-80% of the ESOP pool is going to five or ten senior executives, it raises a fair question:

- Is this a retention tool for the organisation, or an enrichment vehicle for the top floor?

- Insufficient Information to Make an Informed Decision

Institutional investors vote on hundreds of resolutions every year. They rely on the explanatory statement attached to the shareholder notice to understand what they are approving.

If that document is vague, incomplete, or written in a way that leaves out critical details about who gets the options, at what price, under what conditions, they cannot make an informed decision.

Voting against, in such cases, is not a rejection. It is a signal: Investors need more information before they can say yes.

3. The Company’s Point of View: Why they Believe that they are Right

Companies that have their ESOP resolutions voted against often feel confused or even frustrated. From where they stand, they have done everything right.

- Full Legal Compliance

Companies point out that their ESOP schemes are designed in full compliance with SEBI (Share based Employee Benefits and Sweat Equity) Regulations, 2021. The explanatory statement contains all the disclosures required by law. The ESOP scheme has been reviewed by the Nomination and Remuneration Committee, approved by the Board of Directors, and placed before shareholders of the Company

So, when a large chunk of institutional investors still votes against, it can feel deeply unfair.

- Industry Practice Is Being Followed

Companies often highlight that under the SEBI SBEB Regulations, the Nomination and Remuneration Committee has the discretion to determine the exercise price. However, even where a scheme is legally compliant, institutional investors may oppose it if they believe it does not adequately safeguard shareholder interests.

- The Purpose of ESOPs is Genuine

Companies genuinely believe in ESOPs as a human resource tool. They are trying to retain talent, especially in competitive industries where good people have many options. They are trying to build a culture where employees care about the company’s long-term success. Companies want their people to feel like stakeholders, not just employees.

- Annual Disclosures Are Already Being Made

Companies also note that SEBI requires them to disclose detailed information about ESOP grants, vesting, and exercises in their Annual Reports.

From Company’s perspective, investors who want more information can find it there.

4. Investors vs. Employees: Two Different Relationships with the Company

When an employee receives ESOPs, they become a shareholder in the company but that does not make them the same as an institutional investor. The relationship is fundamentally different and that difference matters.

ESOPs give employees a sense of ownership — a feeling that they are building something for themselves too, not just for the company. It is part of why ESOPs work as a retention and engagement tool.

However, it is very different from what an institutional investor wants. They have deployed capital on behalf of thousands of beneficiaries — pensioners, policyholders, mutual fund investors. They are accountable to those people. They need returns and transparency from the Company. They need to know that every share issued is justified.

So, when an investor questions an ESOP scheme, they are not saying employees do not deserve to benefit. They are saying: “We need to understand this better, and the terms need to be fair to all shareholders.”

5. What Can Be Done?

- What Companies Can Do

Most investor concerns can be addressed without changing the substance of the ESOP scheme.

Often, the issue is not what the company is doing, it is how clearly they are explaining it.

a. Focus on What Investors are Actually Reading

Most retail shareholders and even some institutional analysts focus on the resolution text itself but experienced governance practitioners know the real information is in the Explanatory Statement attached to the Notice.

The Explanatory Statement, in accordance with SEBI’s prescribed disclosure format, must contain:

- Preamble — A detailed overview setting out the background and context of the ESOP Scheme.

- Purpose of the scheme — Is it for retention, attraction, or reward?

- Total number of options — What is the maximum possible dilution?

- Employee eligibility criteria — Is coverage broad-based or restricted to senior management?

- Vesting requirements — Is vesting time-based, performance-based, or a hybrid?

- Vesting period — Typically 3 to 5 years in the Indian context

- Exercise price — At market price, or at a discount? If so, how much will be the discount?

- Exercise period—Typically 1-2 years from the date of Vesting.

- Maximum options per employee — Does any single individual receive a disproportionate share?

b. Write a Meaningful Preamble

The preamble of the explanatory statement is the first thing an investor reads. Instead of treating it as a legal formality, companies should use it to tell a story:

- Why is this ESOP Scheme being introduced?

- What problem does it solve?

- What does the company hope to achieve — better retention, wider employee engagement, alignment with long-term goals?

- The compensation and retention strategy.

- How much dilution will occur if all options are exercised? (post-dilution impact)

This kind of transparency builds trust.

c. Design Separate Schemes for Different Employee Groups

Instead of one large ESOP pool that gets distributed broadly, companies may consider designing separate schemes for different levels of employees — senior leadership, middle management, and junior or operational staff.

This approach has several advantages:

- It shows the company thinks about all employees, not just the top floor.

- It allows for different terms that are appropriate to each group.

- For example: performance-linked vesting for senior leaders, and time-based vesting for junior employees who may have less direct influence on financial outcomes.

- When resolutions are tabled separately, investors can support the broad-based scheme even if they have concerns about the senior leadership scheme. This reduces blanket voting against everything.

d. Explain the Exercise Price and Discount Clearly

If the exercise price is at a discount to market, do not just disclose the number, explain the reasoning.

- Is it to attract talent in a competitive market?

- Is it to compensate for lower fixed salaries?

- Is it linked to the risk employees take by joining an early-stage company?

A sentence of context can make a significant difference.

e. Link Vesting to Performance Where Possible

Pure time-based vesting is not wrong, but adding a basic performance condition like the company achieving a minimum revenue target or the employee receiving a satisfactory appraisal rating signals that the scheme is about rewarding value creation, not just tenure.

f. Engage with Investors Before the Shareholder’s Meeting

Large institutional investors are open to engagement. If a company reaches out before the shareholder meeting to explain their ESOP rationale and address questions, they are far more likely to receive a supportive vote. Waiting for the meeting and then being surprised by opposition is avoidable.

- What Institutional Investors Can Do

Institutional investors also have a role to play in making this process more constructive.

- When voting against a resolution provide specific written feedback to the company about what was missing or unclear. Generic opposition without guidance does not help companies improve.

- Recognise that a company following all legal requirements deserves acknowledgment, even if the disclosure could be better. Voting against a fully compliant scheme without engagement can feel unfair.

- Engage with companies proactively. If the same concerns come up year after year, direct engagement is more useful than annual negative votes.

Conclusion

- The tension around ESOP resolutions is not about companies acting in bad faith or investors being overly demanding. Rather, it reflects two stakeholders with different roles, responsibilities, and perspectives trying to make a shared decision on a complex issue.

- Companies use ESOP schemes to attract, motivate, and retain talent while complying with the law in both letter and spirit.

- At the same time, institutional investors seek to safeguard the capital of millions of ordinary investors by promoting greater transparency and accountability.

- The gap between them is real, but it is bridgeable. Better disclosure, more thoughtful scheme design, and genuine engagement can go a long way.

- When companies explain their ESOP schemes clearly and investors respond constructively, the outcome is better for everyone that are employees, shareholders, and the company as a whole.

The goal should not be to win a shareholder vote. The goal should be to earn trust and keep it.